How to Do a 1031 Exchange Successfully

With proper planning, have a successful exchange instead of a taxable problem.

Property Title

To qualify as an exchange under Internal Revenue Code Section 1031, your replacement property has to be owned by the same taxpayer that owned the relinquished property.

Typically, this means the owner or ownership entity that begins the exchange, or relinquishes property, has to be the entity that acquires the replacement property.

Qualified Intermediary’s Role

The exchange documents prepared by your qualified intermediary (QI) will mirror the ownership (or vesting) information of the title or preliminary title report issued for your relinquished property. For example:

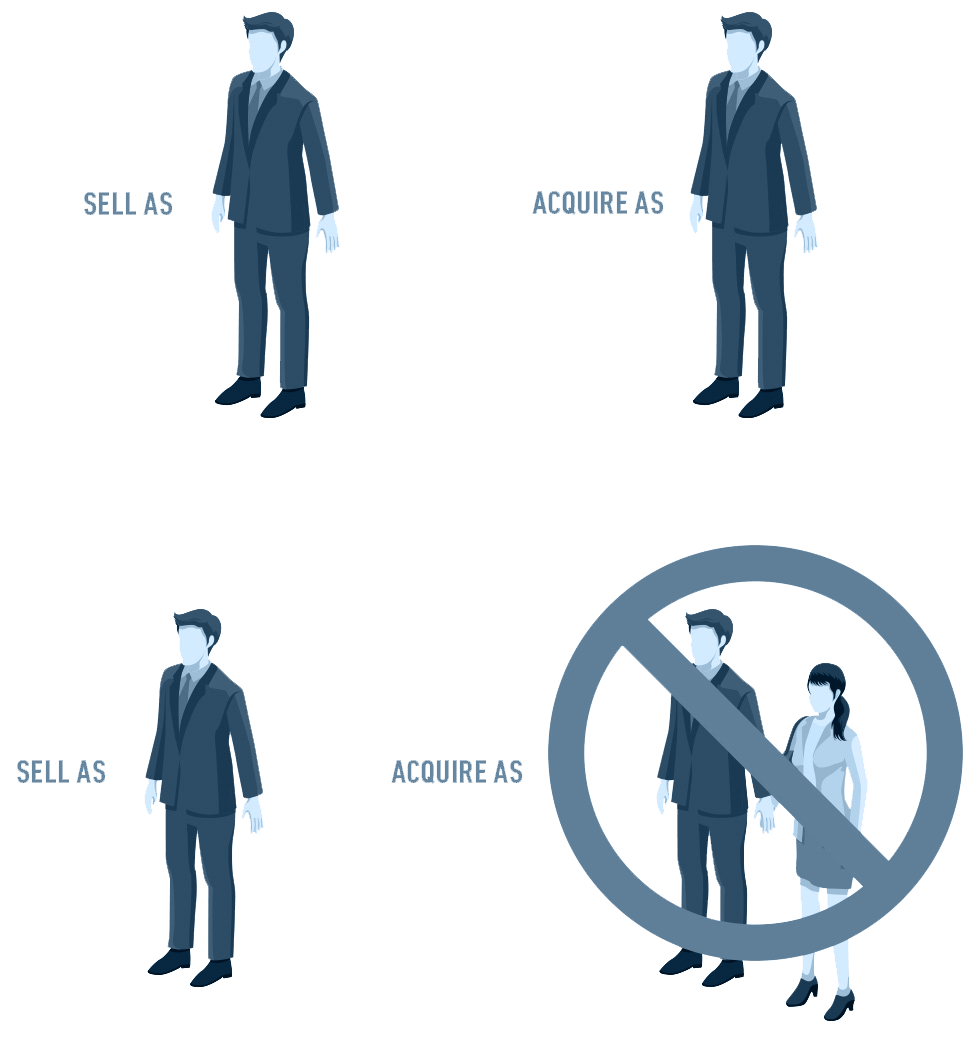

- If you sell as an individual, you need to acquire as an individual.

- If you sell as a married couple, you need to acquire as a married couple.

- If you sell as a corporation, you need to acquire as the same corporation.

- If you sell as a partnership, you need to acquire as the same partnership

Your QI holds sale proceeds while you locate your replacement property. Your QI also helps document the exchange.

Exceptions to Consistent Ownership

Generally, ownership must stay the same or the exchange is invalidated. In some states—not all—exceptions allow for name changes while keeping the “same taxpayer,” without invalidating the exchange. For example:

- If you sell in the name of a revocable living trust, you may be able to acquire the replacement property in the trustor’s individual capacity.

- Certain revocable living trusts may be disregarded for federal tax purposes. So, although a different name, since the trust may be “disregarded,” its trustor was always the taxpayer, and remains so in the trustor’s own name.

- If you sell as an individual (or married couple, if governed by community property laws), you may be able to acquire replacement property in a single-member limited liability company (LLC), which can be disregarded for federal tax purposes.

- The acquisition of a disregarded single-member LLC that owns the replacement property is treated as an acquisition by the single member.

Anticipate Issues

Anticipate ownership issues. Issues are easier to solve before contracts and loan documents are prepared and you’re ready to close. Understand that business considerations, liability issues and lender requirements can make it difficult to keep the same ownership on your replacement property.

Avoid making any changes in ownership to the relinquished or replacement properties before or during the exchange. If you do, the IRS may disqualify the holding use as for resale, and your exchange disqualified.

Consult your tax or legal advisor about how ownership issues can impact the structure of your exchange before your transfer your relinquished property.